The battery backlash: China's EV dilemma

In the gleaming showrooms of Shenzhen and Shanghai, Chinese electric vehicles hum with the quiet confidence of technological superiority. BYD, Chery, and a constellation of lesser-known manufacturers have achieved what seemed improbable a decade ago: they have surpassed Western rivals in battery technology, manufacturing scale, and price competitiveness. China now accounts for more than 70% of global EV production and around the same share of battery capacity. Yet as these electric dragons prepare to conquer foreign markets, they face an inconvenient truth. The world is not as welcoming as China's domestic market once was to foreign entrants.

The irony is sharp. When Western manufacturers sought access to China's vast market in the 1990s and 2000s, they accepted terms that would have made nineteenth-century treaty negotiators blush. Joint ventures with local partners were mandatory. Technology transfers were expected. Manufacturing had to be local. These conditions, though commercially painful, were the price of admission to what would become the world's largest automotive market. The strategy worked spectacularly—for China. European and American firms taught their Chinese partners everything from engineering fundamentals to supply chain management, effectively training the competition that now threatens their survival.

Today, as Chinese manufacturers look westward with similar ambitions, they face calls for reciprocity that they seem unwilling to entertain. The European Union, once the champion of free trade and open markets, increasingly sounds like Beijing circa 2005. "Demand local production in exchange for market access," runs the refrain. "Require joint ventures with domestic partners." The wheel has come full circle, except China shows little appetite for turning.

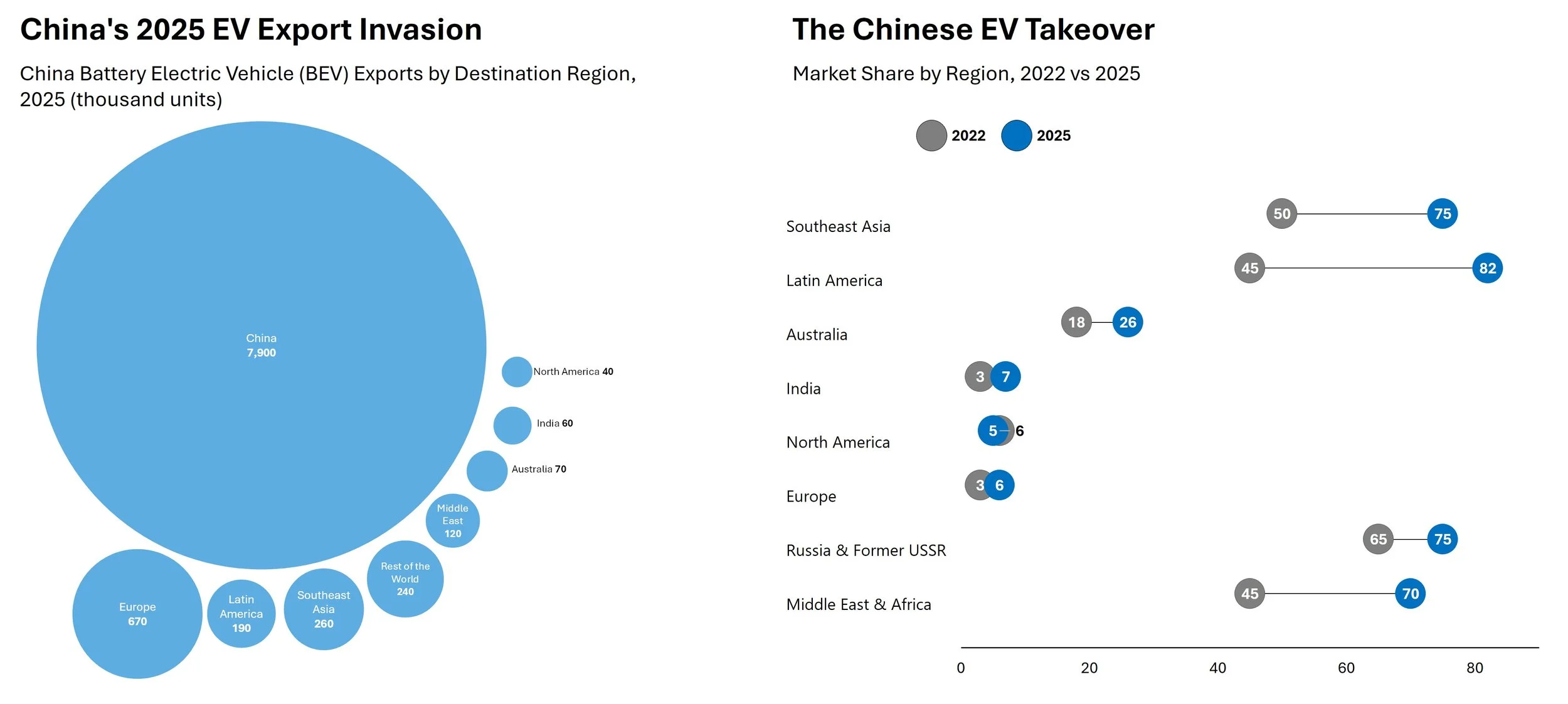

This reluctance creates a strategic bind. China's EV industry, despite its technological achievements, faces overcapacity at home. Domestic sales, though substantial at around 20-30% in 2025, cannot alone absorb the productive capacity that has been built. Exports—which surged to around 1.5-2m pure EVs in 2025—are not merely desirable; they are essential. Yet the very advantages that make Chinese EVs competitive—government subsidies, vertically integrated supply chains, and economies of scale achieved through protected domestic markets—are precisely what provoke protectionist responses abroad.

The United States has already shown the way forward, or backward, depending on one's perspective. Donald Trump's administration has weaponised tariffs with abandon, effectively barring Chinese EVs from American roads. Europe, traditionally more circumspect about trade barriers, finds itself pulled in the same direction. The recent struggles of legacy manufacturers—Volkswagen's profit warnings, Stellantis's stumbles, even Porsche's miscalculated EV bet—create political pressure for protection. When factories face closure and workers face unemployment, free trade principles become negotiable.

This leaves China with three imperfect options, none particularly palatable. The first is to seek alternative markets—Southeast Asia, Latin America, Africa—where protectionist sentiment is weaker and infrastructure needs are greater. Yet these markets lack the purchasing power of Europe and America. They can absorb some excess capacity but cannot replace the rich-world consumers who can afford premium electric vehicles.

The second option is a strategic retreat reminiscent of Japan's voluntary export restraints in the 1980s. When Japanese cars flooded American and European markets, Tokyo chose accommodation over confrontation, limiting exports to preserve market access. China could follow this script, accepting quantitative restrictions in exchange for avoiding outright bans. This would preserve some market share while reducing the political temperature. Yet it runs counter to Beijing's industrial ambitions and would leave substantial capacity underutilised.

The third option is to play hardball—maintain current export strategies and dare Europe to follow America's protectionist path. This gamble assumes European political will for trade barriers is weaker than the rhetoric suggests, that consumers' desire for affordable EVs will override manufacturers' pleas for protection. It is a risky wager. Europe has shown surprising unity on China policy recently, and the political costs of being seen as soft on Beijing may outweigh economic logic.

The uncomfortable reality for China is that all three paths lead through difficult terrain. The Japanese precedent offers lessons: voluntary restraint preserved market access but also spurred Japanese manufacturers to build local production facilities in America and Europe, transferring some technological advantage in the process. Toyota and Honda became quasi-domestic producers, their "foreign" identity gradually fading. China could follow this model, but it would require accepting the very conditions—local partnerships, technology sharing—that Beijing sought to avoid.

The broader question is whether the era of China's asymmetric market access is ending. For two decades, Western firms accepted unfavorable terms in China while Chinese firms enjoyed relatively open access to Western markets. This arrangement was tolerable when China was catching up. Now that Chinese firms lead in crucial technologies like batteries, the political sustainability of the arrangement has evaporated.

What is emerging instead resembles "Globalisation 2.0," as some commentators describe it—a world where market access is explicitly traded for local production, technology transfer, and job creation. The difference from the original globalisation is the frank acknowledgment that these are quid pro quo arrangements rather than expressions of free trade principle.

For China's EV industry, this represents a moment of truth. Its technological achievements in battery chemistry, manufacturing efficiency, and integration are genuine. CATL's lithium iron phosphate batteries and BYD's blade battery design represent real innovations, not mere copies. Yet technology alone does not guarantee market access, as many Chinese officials are discovering. Politics, as it turns out, still trumps economics—even in an industry meant to save the planet.

The resolution of this dilemma will shape not just the automotive industry but the broader template for managing technological competition between China and the West. If Chinese manufacturers accept local production requirements and genuine partnerships, they might preserve market access while contributing to European and American industrial renewal. If they resist, they risk being shut out of the world's wealthiest markets entirely.

The EV revolution was supposed to transcend geopolitics, uniting the world in common cause against climate change. Instead, it has become another arena where technological leadership, economic nationalism, and strategic rivalry collide. China built the better battery. Now it must navigate the even more complicated challenge of making the world willing to buy it.■