The Pill Problem: How the West handed the keys to its medicine cabinet

In the spring of 2025, as American factories ground to a halt for want of rare-earth minerals, President Donald Trump discovered what strategic dependency truly means. China had choked off supplies, forcing the world's most powerful nation to the negotiating table. Yet rare earths may be the appetiser. The main course sits in millions of bathroom cabinets: pills that keep hearts beating, infections at bay, and blood pressure under control.

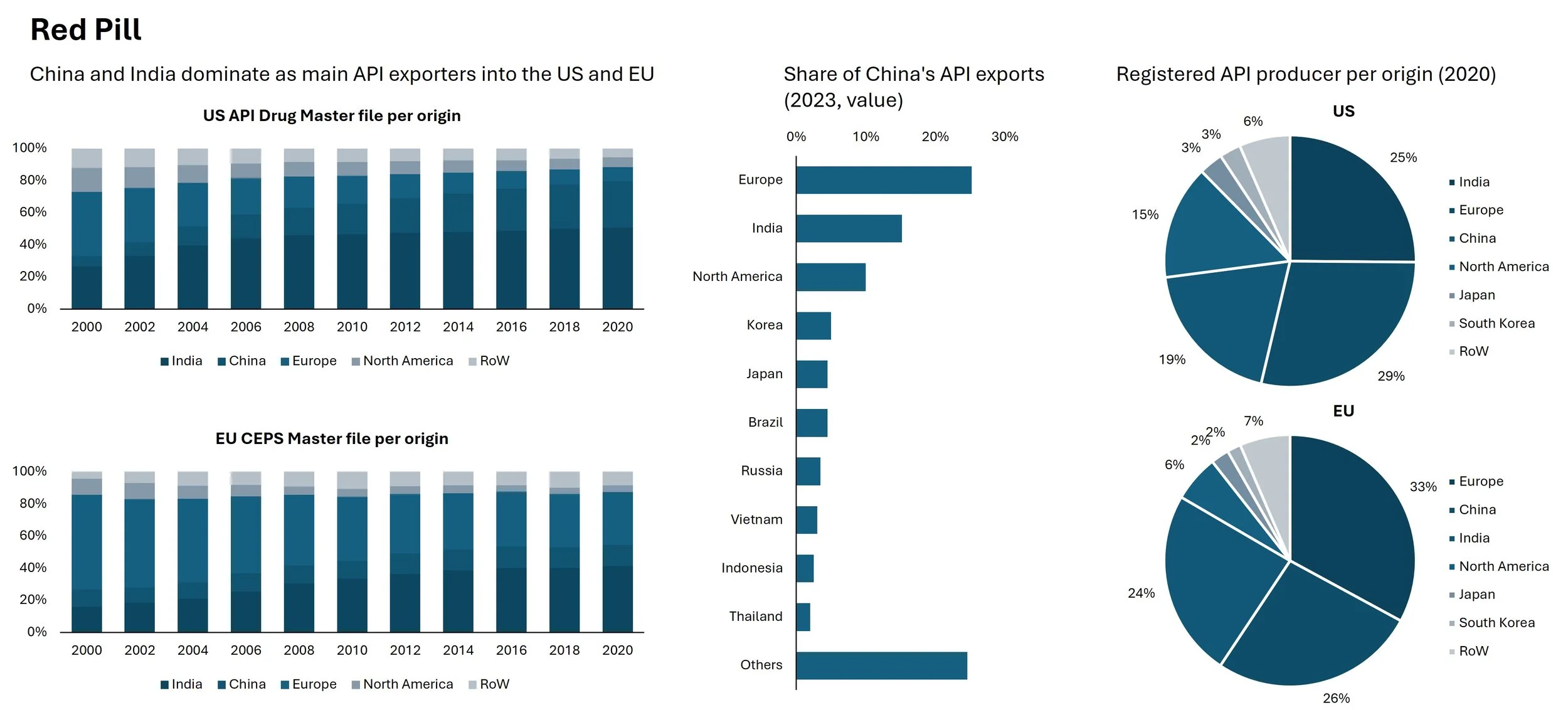

Western healthcare systems face a vulnerability so profound that defence officials speak of it as a military threat. Some 74% of the active pharmaceutical ingredients (APIs) that Europe requires come from Asia—principally China and India. For the United States, the figure reaches 60% when accounting for India's own dependence on Chinese raw materials. This is a chokepoint that could be weaponised in conflict, with consequences measured in human lives.

Regulators cling to the illusion that India offers a hedge against Chinese dominance. They are mistaken. India depends on China for 68-70% of its imported APIs and drug intermediates, and for most of its key starting materials—the deepest layer of the supply chain. Indian pharmaceutical exports are, in effect, Chinese products with an Indian processing step. Shifting procurement from Shanghai to Mumbai changes nothing —it just hides the dependency behind another layer of invoicing.

The scale of this dependency would have seemed inconceivable a generation ago. In 2000, European manufacturers held 59% of all certificates for pharmaceutical ingredients; Asia claimed just 35%. By 2020, the positions had reversed: Asia commanded 63%, Europe a mere 33%. Europe's share of new API registrations collapsed from 42% in 2000 to just 10% in 2023. For 93 essential ingredients, there is now no European production whatsoever.

How did the West sleepwalk into such strategic fragility? The answer lies in a potent cocktail of cost pressure, regulatory arbitrage, and wilful blindness.

The exodus began in the 1990s, driven by procurement systems awarding contracts almost exclusively on price. Germany's "winner-takes-all" tenders forced generic manufacturers into a race to the bottom. Asian APIs cost 20-40% less than European equivalents, thanks to lower labour costs, minimal environmental enforcement, state subsidies, and economies of scale. Europe's stringent regulations imposed additional costs of 20-30%—without equivalent import requirements.

China played a longer game. Through "Made in China 2025", Beijing systematically supported pharmaceutical development. The result was steady European exits. The last paracetamol plant on the continent closed in 2008. Novartis's Kundl facility remains the lone fully integrated antibiotics production site in the Western world.

Covid-19 should have been the wake-up call. Yet January 2026 data reveal the dependency has deepened. China surpassed India in new API registrations in 2024 for the first time in two decades, capturing 45%. Europe's share languishes at 6%; America's at 3%.

In May 2025, Xellia Pharmaceuticals announced it would close its Copenhagen plant and shift production to Hungary and to China. "Otherwise, not just 80% of the APIs will come from China, but close to 100% very soon." Half of Xellia's products feature on the EU's critical medicines list. The current economic model strangles European investment in generic medicines.

What makes this especially dangerous is how little Western governments know. The U.S. Food and Drug Administration lacks data on actual API import volumes. Drug Master Files show capacity, not production. For key starting materials, data is scarcer still.

The Pentagon designated 27% of essential medicines as "very high risk", including 5% from China and 22% from unknown countries. The Strategic Reserve stood at 1% of its two-year target as of March 2024. EU authorities reported 136 critical medicine shortages between 2022 and October 2024.

Concentration amplifies the danger. Production clusters in just four states in India and four provinces in China. A 2016 explosion at one Chinese factory caused worldwide piperacillin shortages.

Can China weaponise this dependency? The precedent is disturbing. In 2020, Xinhua suggested that if China restricted medical exports, America would be "trapped in the vast ocean of Covid-19." A Tsinghua economist urged export controls on vitamins and antibiotic materials to "halt global medical systems." Xi Jinping wrote that China must "tighten the dependence of international industrial chains on our country to deter others from hurting China"—whilst claiming supply-chain control "shouldn't be weaponised."

The 2025 rare-earths episode proved Beijing's willingness to deploy such leverage. "The pharmaceutical industry represents a sector that is possibly at greater vulnerability than that of rare earths.

China could escalate in stages. A direct cutoff would eliminate 13% of U.S. APIs immediately. But the real leverage lies deeper: restricting key starting materials to India—for which China supplies 68-70% of imports—could threaten up to half of U.S. generic drug supply. This would force New Delhi into an impossible choice between domestic needs and export commitments, exposing the folly of treating Indian supply as independent from Chinese control.

Constraints exist. Restricting pharmaceutical exports would damage China's reputation and industry. But as rare earths demonstrated, Beijing accepts such costs when strategic interests are at stake.

This dependency doesn’t just threaten national security—it endangers lives. FDA inspections in China are pre-announced—unlike domestic unannounced visits. Since the pandemic, Chinese sites have refused 150 FDA inspection requests. China's anti-espionage laws have caused German inspectors to refuse travel for fear of arrest. The valsartan scandal saw Chinese ingredients contaminated with a probable carcinogen, affecting millions worldwide.

This is the bargain Western healthcare struck: cheaper medicines for reduced oversight and heightened vulnerability. As an EU official said, drawing a parallel to Russian gas: "When it's cheap and flowing, it's great for your industry. Until it doesn't, and then it's really expensive."

Why has reshoring proved so elusive despite five years of policy dialogue? China's advantages are "sub-rational": state-subsidised utilities, state-bank loans to loss-making companies, minimal environmental protections, and giant integrated chemical parks. India's own USD 1bn reshoring programme, launched in 2020 to reduce dependency on Chinese inputs, has largely failed; Chinese firms still offer prices half as costly for certain drugs. If India—with lower costs and established pharmaceutical infrastructure—cannot break free, Western prospects look bleak.

European pharmaceutical companies are moving production into China, not out. A European Chamber of Commerce survey found 80% shifting more manufacturing eastward, driven by local content requirements. Moving just one antibiotic group's production back to Europe would cost EUR 55m—multiply that across hundreds of essential medicines, and the bill becomes politically unpalatable.

China's ambitions now extend beyond commodity chemicals to cutting-edge innovation. Clinical trial enrolment proceeds 2-5 times faster than in the West. China leads in synthetic biology, positioning itself to dominate mRNA technologies. Its biotech capabilities "rival those of top Western nations," according to a U.S. Senate report.

Europe's proposed Critical Medicines Act aims to improve procurement and strengthen supply chains. Austria and Novartis invested EUR150m to secure the Kundl plant. But such measures feel, too timid and taking too long.

The West’s pharmaceutical dependency is a crisis waiting to happen. Western healthcare systems were built on cheap medicines enabled by Asian production, yet the political will to pay more for supply security has not been tested against constrained health budgets. An old Soviet joke comes to mind: "We pretend to work, and they pretend to pay us." In pharmaceuticals, the West pretends to address the dependency whilst Asia pretends the relationship is purely commercial. Such pretences rarely survive contact with crisis. Like Europe’s reliance on Russian gas, the benefits of cheap medicines will seem trivial once the supply stops. The rare-earths shock of 2025 was a warning. The next crisis may not be negotiable—and the cost will be measured in lives, not dollars. The time to act is now, before the cabinet goes dark.■