Solid energy: Losing the aluminium loop

In an industrial park in Cassopolis, Michigan, Norsk Hydro operates a facility that represents the West's best hope for aluminium self-sufficiency. The plant processes 7 thousand tonnes of scrap metal monthly—old beverage cans, automotive trim, demolished window frames—melting them down into fresh aluminium. Recycling requires only 5% of the energy needed to produce primary metal from bauxite ore, making it economically viable even with America's electricity prices. Yet this success story contains a troubling paradox. The very scrap that feeds such plants is increasingly flowing abroad, snapped up by Chinese and American buyers willing to pay premium prices. Europe, which pioneered sophisticated recycling systems, now faces the prospect of becoming a net exporter of the raw material its own industry desperately needs.

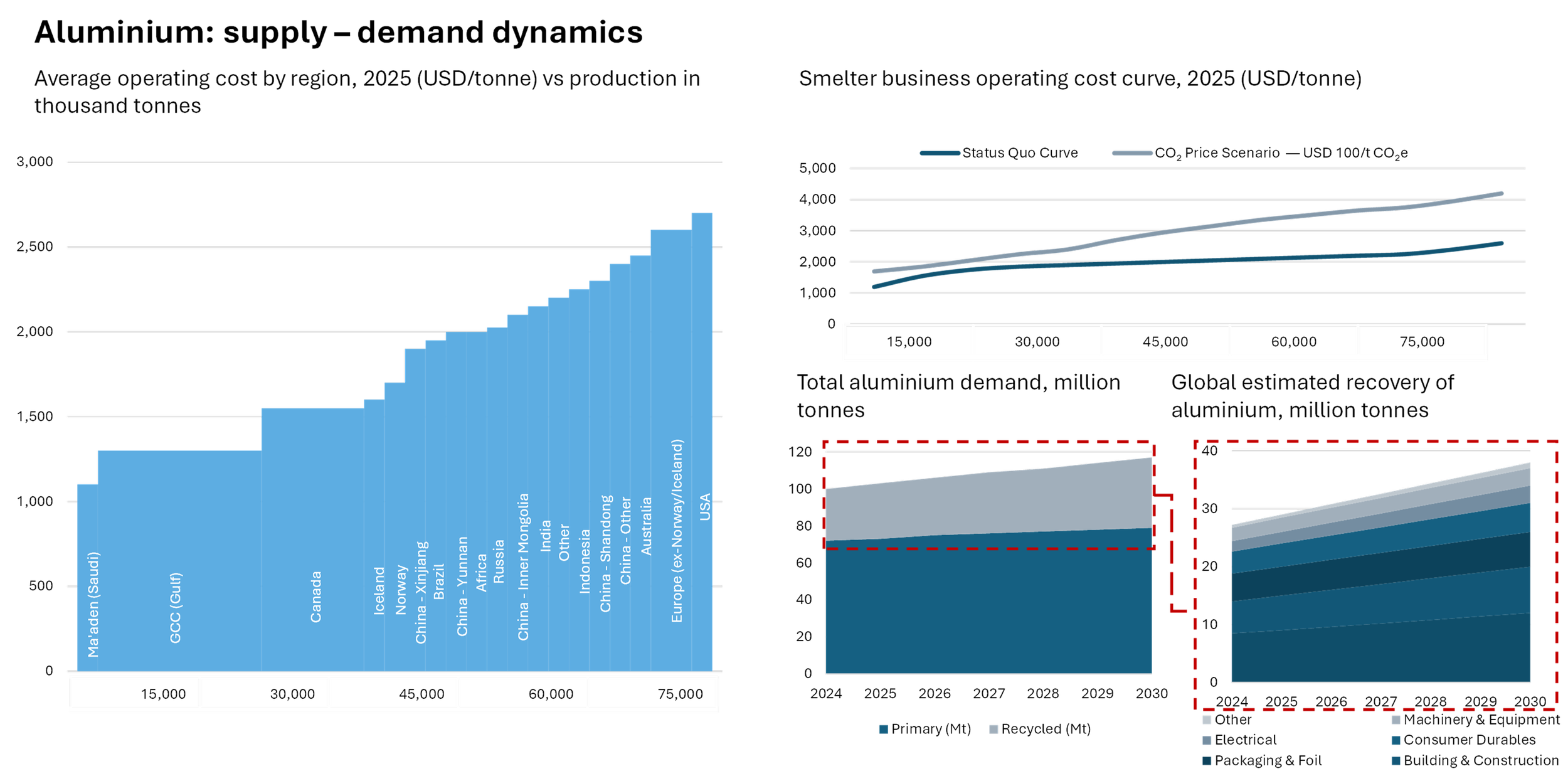

The eastward migration of aluminium production represents one of modern industry's starkest geographical shifts. China's share of global output has surged from roughly 8% in 2000 to 60% today—some 43 million tonnes annually. This dominance stems from a simple equation: aluminium smelting is phenomenally energy-intensive. Producing a single tonne requires approximately 13-14.5 MWh of electricity, equivalent to what five German households consume in a year. Industry insiders call the metal "solid electricity", and with good reason. When energy costs diverge dramatically between regions, production inexorably follows the cheapest electrons.

China's ascent was built on captive coal-fired power plants constructed specifically for aluminium production. Companies like China Hongqiao Group secured electricity at rates far below both Chinese grid tariffs and international benchmarks by building their own infrastructure in coal-rich provinces such as Shandong and Inner Mongolia. Even today, over half of China's captive aluminium power capacity relies on subcritical coal combustion—less efficient but extraordinarily cheap. Government support amplified this advantage through concessionary loans, tax rebates on exports (until their removal in November 2024), and electricity subsidies from regional authorities eager for industrial development.

Europe, by contrast, operated on a fundamentally different model. Historically, smelters secured long-term power purchase agreements tied to hydroelectric or nuclear baseload capacity. Norway and Iceland, blessed with abundant hydropower, remain competitive. But Russia's invasion of Ukraine in February 2022 shattered the broader European industry. Dutch TTF gas prices spiked from approximately EUR 30 per MWh before the crisis to EUR 345 in August 2022—an eleven-fold increase. Although prices have since retreated to EUR 75-100, this remains well above the EUR 30-40 threshold required for profitable smelting. The casualty list is extensive: Speira's Rheinwerk plant in Germany, Aldel's Farmsum smelter in the Netherlands, Slovalco in Slovakia, Talum in Slovenia, Alcoa's San Ciprián works in Spain. Europe suspended approximately 1.4 million tonnes of annual capacity between late 2021 and 2022. Roughly 800,000 tonnes remains idle today.

American smelters face a different but equally intractable constraint: competition from artificial intelligence. Data centres are willing to pay USD 115 per MWh or more for dependable round-the-clock power—nearly three times what an aluminium smelter can afford. Microsoft's reported commitment to pay Constellation Energy this rate to restart the Three Mile Island nuclear plant exemplifies the phenomenon. The US Aluminium Association warns bluntly that technology companies have "no limit on what they are prepared to pay for dependable electricity". A modern 750,000-tonne smelter consumes more electricity than a city the size of Boston. Competing against virtually unlimited AI budgets, primary aluminium production in America has collapsed from 24 operating plants in 2000 to just 4 today.

With primary production economically unviable, the West pivoted to recycling. The logic seemed impeccable: secondary aluminium requires only 5% of the energy input, largely bypassing the electricity cost disadvantage. Europe developed the world's most sophisticated collection infrastructure, recovering approximately 70% of beverage cans compared with 40% in America. This should have provided strategic advantage. Instead, it has become a vulnerability.

European scrap is haemorrhaging abroad. Exports reached 1.3 million tonnes in 2024—a 53% increase since 2019. Approximately 75% flows to Asia, with China the primary destination. In the first quarter of 2025, exports to America surged 273% year-on-year as US buyers sought feedstock to circumvent President Donald Trump's 50% tariffs on finished aluminium (scrap itself remains exempt). Chinese buyers can afford premium prices because subsidised domestic overcapacity and quarter-the-price electricity costs allow them to import European scrap, remelt it using coal-fired power, and export finished products back to Europe. The result: approximately 15% of EU recycling furnace capacity now sits idle due to insufficient feedstock—a shortfall of roughly 2 million tonnes annually. As voices from the industry put it: "We have lost primary production. Now we are at risk of losing aluminium scrap."

The policy response has been characteristically fragmented. The EU announced in November 2025 that it would introduce measures to address "scrap leakage" by spring 2026, potentially including export levies of 25-30%. American tariff architecture, meanwhile, has created perverse incentives. By exempting scrap from the 50% levy applied to refined aluminium, Washington has encouraged domestic fabricators to import feedstock rather than finished metal. The US Midwest premium—the surcharge buyers pay above London Metal Exchange prices—has tripled in 2025, exceeding USD 1 per pound (USD 2,200 per tonne) for the first time. American warehouses linked to the LME now hold precisely zero aluminium, having been completely depleted.

China's dominance contains a structural constraint. In 2017, Beijing imposed a production capacity cap of 45 million tonnes annually to control energy consumption and limit emissions. By 2025, Chinese output had reached this ceiling, meaning the country can no longer single-handedly supply the world's incremental demand, which runs at 2-3 million tonnes per year. This has pushed Chinese companies to replicate their model offshore, primarily in Indonesia.

The archipelago offers abundant bauxite reserves, cheap coal-fired electricity, low labour costs, and a government eager to move downstream in commodity processing. Eleven planned smelters could add approximately 13 million tonnes of capacity, with Chinese firms accounting for 84% of investment. Indonesian production is estimated could quintuple by 2030, potentially making it the world's fourth-largest producer. This mirrors China's earlier transformation of Indonesia's nickel industry, where similar offshore expansion created global dominance. Yet aluminium faces headwinds that nickel did not: higher construction costs, power infrastructure constraints, and policy uncertainty following China's 2021 pledge to cease funding overseas coal projects. Whether Indonesia can truly replicate the nickel playbook remains contested.

The industry's eastward shift undermines Europe's climate ambitions in ways that official statistics obscure. Every tonne of aluminium produced in China using coal-fired electricity emits approximately 15 tonnes of carbon dioxide. European production, largely powered by hydro and nuclear, emits under five tonnes per tonne of metal. By allowing domestic smelters to close and replacing their output with Chinese imports, Europe has exported rather than reduced emissions. The EU's Carbon Border Adjustment Mechanism, which entered force on January 1st 2026, theoretically addresses this by pricing imported carbon. But full implementation—requiring complete phase-out of free emissions allowances—will not occur until 2034. For nearly a decade, European producers generating two-thirds less carbon than Chinese counterparts will remain at a competitive disadvantage.

The strategic implications extend beyond climate accounting. Europe's energy transition requires an additional 4 million tonnes of aluminium annually by 2030, rising to 5 million tonnes by 2040—equivalent to 30% of current consumption. Electric vehicles, solar panels, and grid infrastructure all depend on a metal whose supply chains are now predominantly controlled by Chinese companies, whether operating domestically, in Indonesia, or elsewhere. Critical materials for decarbonisation flow through jurisdictions outside European control. As EU Trade Commissioner Maroš Šefčovič acknowledged: "Europe's future will to a large extent depend on its ability to secure access to the raw materials that our economy and our society require."

The aluminium market faces a binary outcome: either higher prices spilling across the global economy, or deepening reliance on Chinese companies. Most probably, both will occur simultaneously. Prices are already trading near three-year highs at USD 3,300 per tonne, with forecasts of structural deficit extending through 2027. For Europe, the policy options grow narrower. Export controls on scrap may slow outflows but cannot address the fundamental energy cost disadvantage. Accelerated carbon border implementation could level the playing field, but political appetite for measures that would raise consumer prices appears limited. Long-term industrial electricity contracts for surviving smelters would require state intervention in power markets that policymakers have spent decades liberalising.

What has emerged is perhaps the sharpest illustration of how environmental policy, trade policy, and industrial competitiveness intersect in strategic commodity markets. Europe's carbon pricing, implemented without adequate border protection, destroyed its cleanest producers first. America's tariff architecture, by exempting scrap, accelerates the very import dependency it ostensibly addresses. China's capacity cap, meant to curb emissions and overcapacity, has merely pushed production to Indonesian coal plants that will emit just as prodigiously. The result is an industry in what Novelis describes as "terminal decline"—expensive, carbon-intensive, and controlled by entities outside Western jurisdiction. Reversing this trajectory would require co-ordinated industrial policy on a scale that shows little sign of materialising. The West is discovering that losing an industry is far easier than rebuilding one, particularly when the barrier to entry is measured not in capital or technology, but in gigawatt-hours of affordable electricity that no longer exist. ■